In Focus: Singapore | By Hok Yean Chee

In Focus: Singapore

Source: HVS Research |

In Focus: Singapore

Source: Economist Intelligence Unit (EIU), January 2025 |

In Focus: Singapore

Source: HVS Research |

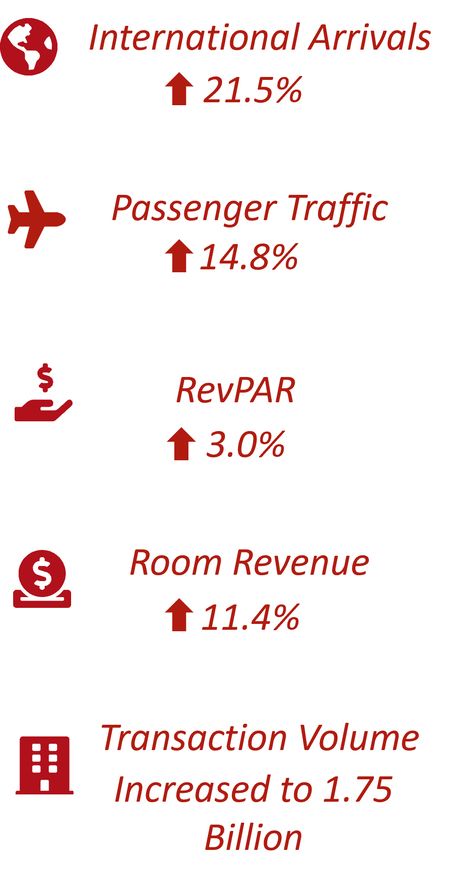

Key Highlights in 2024

Singapore, a city-state spanning 734 square kilometres with a population of approximately 6.04 million, remains one of the world’s top travel and business destinations. Its modern infrastructure, cultural diversity, and strategic location continue to attract millions of visitors annually.

In 2024, Singapore’s tourism sector saw strong growth, with international arrivals rising by 21.5% compared to the previous year. Passenger traffic increased by 14.8%, bringing it just under 1.0% below 2019 levels. The hospitality industry also performed well, with revenue per available room (RevPAR) up 3.0%, while total hotel transaction volume climbed to SGD1.75 billion..

The resurgence of large-scale events and entertainment played a key role in driving tourism. Major concerts by global artists such as Taylor Swift and Coldplay drew visitors from across the region, while marquee events like the Formula 1 Singapore Grand Prix and Singapore Art Week further boosted arrivals. Despite positive trends, visitor numbers from key markets, including China and Indonesia, have yet to fully recover to pre-pandemic levels.

Looking ahead to 2025, Singapore’s tourism sector is expected to maintain its upward trajectory, supported by increasing flight connectivity and a robust calendar of international events. Continued investments in attractions and hospitality infrastructure will be crucial in sustaining growth, positioning the city-state for another strong year in tourism.

|

In Focus: Singapore

Source: HVS Research |

Economic Outlook

In 2024, Singapore's economy saw a strong recovery, with GDP growth rising to 3.8% from 1.1% in 2023. This was driven by robust domestic demand, improved global trade, and strength in key sectors like finance and advanced manufacturing. The budget balance returned to a surplus of 0.2% after years of deficits.

Looking ahead, GDP growth is expected to stabilise between 2.4% and 2.6% annually from 2025 to 2029. Lending interest rates, which peaked at 5.5% in 2023, are set to gradually decline, supporting investments. With ongoing initiatives in digitalisation and sustainability, Singapore’s diversified economy remains well-positioned for long-term resilience despite external uncertainties.

Figure 1: Economic Outlook

|

In Focus: Singapore

Source: Economist Intelligence Unit (EIU), January 2025 |

Economic Performance & Outlook

Singapore remains a leading Asian economy, with GDP projected to grow 2.5% in 2025, moderating from 2024’s 3.8%. While strong domestic demand supports growth, global uncertainties pose risks. A Trump presidency could impact Singapore’s trade, as proposed U.S. tariffs may disrupt exports. Monetary policy uncertainty also looms, with economists split on whether the Monetary Authority of Singapore (MAS) will ease or maintain its stance. To navigate these challenges, Singapore’s focus on innovation, digital services, and sustainability will be key to sustaining long-term economic resilience.

Currency Exchange Outlook

Singapore has historically had a steady exchange rate, however, the Singapore dollar (SGD) is expected to weaken further against major currencies in 2025. Analysts predict this trend due to the MAS recent policy adjustments and ongoing global economic challenges. Additionally, the US dollar's strength and economic recovery in the eurozone continue to exert pressure on the SGD. The exchange rate (SGD:USD) is expected to fluctuate between 1.34 to 1.36 over the next five years.

Inflation

EIU reported that Singapore's inflation rate was 2.4% in 2024, reflecting easing pressures on car prices, clothing, and some food items. Looking forward, the EIU predicts a further reduction to 1.9% in 2025, indicating ongoing moderation in price growth. This rate remains above the pre-pandemic average of 1.7% due to potential increases in import costs from trade protectionism. Nonetheless, the overall moderation in inflation highlights Singapore's robust capability to manage inflation amid global economic challenges.

Interest Rates

Singapore discontinued the Singapore Interbank Offered Rate (SIBOR) at the end of 2024, replacing it with the Singapore Overnight Rate Average (SORA) for greater transparency and reliability. Unlike SIBOR, SORA is based on actual transactions, making it more stable. As of February 2025, the 3-month SORA rate stands at 2.85%, while the 1-month rate is 2.70%. The EIU forecasts Singapore’s lending interest rate to fall from 5.3% in 2024 to 4.8% in 2025, signalling lower borrowing costs, which could stimulate economic growth, investment, and spending.

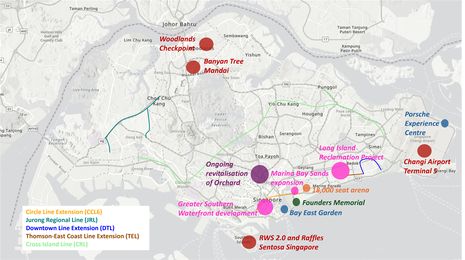

Infrastructure Developments

2025

- Resorts World Sentosa expansion project (RWS 2.0)

- Debut of Mandai Rainforest Resort by Banyan Tree and Raffles Sentosa Singapore

- DT4 Hume opened 28 February

- Changi Airport Terminal 5 to begin construction

- Works to expand Woodlands Checkpoint to begin

2026

- Ongoing revitalisation of Orchard Road to be a lifestyle destination

- TEL Bedok South and Sungei Bedok to open

- DTL Xilin and Sungei Bedok to open in 2H2026

- 4-km CCL6 will close the loop by adding three stations (Keppel, Cantonment and Prince Edward Road), connecting Harbourfront to Marina Bay station

2027

- Bay East Garden to open

- 21.5-km North-South Corridor connecting the northern region to CBD will be completed in phases

- First Regional Porsche Experience Centre to open

- JRL (West) Phase 1 comprises ten stations linking Choa Chu Kang to Boon Lay and Tawas

2028

- JRL Phase 2 to be completed

- Founders’ Memorial to open

2029

- JRL to be fully completed

Beyond 2030

- 12-km Greater Southern Waterfront development (2030)

- Marina Bay Sands 4th tower expansion project (2031)

- Eight MRT line - Cross Island Line (2032)

- DTL extension (2035)

- Completion of Changi Airport T5 (2030s - 2040s)

- Tuas Mega Port (2040)

- Long Island Reclamation project

- 18,000 seat arena replacing Singapore Indoor Stadium

Figure 2: Infrastructure Developments (2025 - 2030 and beyond)

|

In Focus: Singapore

Source: HVS Research |

Additional Contributors to this article: Chariss Kok, Vice President, Jay Low, Manager and Mildred Sim, Analyst.

HVS

https://www.hvs.com/

1400 Old Country Road, Suite 105N

USA - Westbury, NY 11590

Phone: +1 (516) 248-8828

Fax: +1 (516) 742-3059

HVS ANAROCK MONITOR, March 2025

HVS London Expands Asset Management Division

European Hotel Transactions Surge in 2024 Marking a Turning Point for Investment